Where’s the weed!?

That’s been a common Canadian refrain lately. Shortages appeared almost immediately after recreational cannabis sales began last October.

Provincial distributors subsequently blamed producers and federal regulators. Lacking stock, Québec closed stores three days a week. Alberta froze retailer licensing and Ontario limited store licences to 25.

Medical cannabis shortfall concerns appeared even earlier. Some users worried producers were prioritizing more lucrative recreational products or overseas markets.

In response, federal regulators pointed to increasing industry inventories and producer licences. Producers blamed new-industry growing pains and regulatory red tape. Meanwhile, some analysts criticized provincial licensing limits as over-reactions.

How can Canada seemingly have large cannabis supplies and yet widespread shortages? Recently released Health Canada cannabis inventory and sales data provide some clues.

Growing supplies

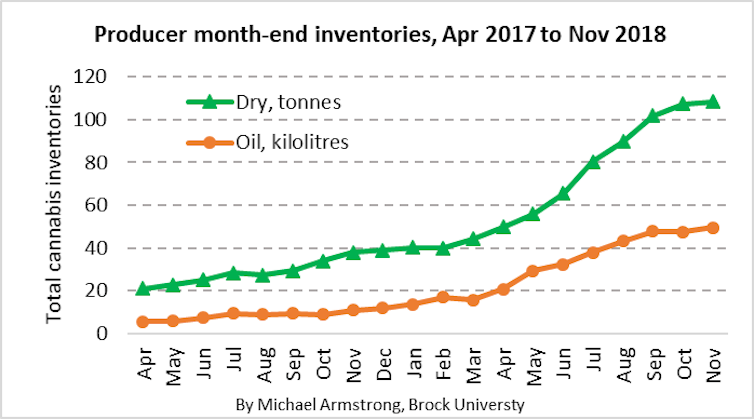

Cannabis producers greatly expanded their stockpiles prior to legalization last year. Between January and September, month-end inventories of “dry” cannabis (flowers and leaves) more than doubled from 40 to 102 tonnes.

Similarly, cannabis-infused oil supplies more than tripled, from 14 to 48 kilolitres. Inventory growth slowed in October as recreational sales began.

So as officials have noted, there was lots of cannabis overall. That doesn’t mean there weren’t shortages.

Medical decline and rebound

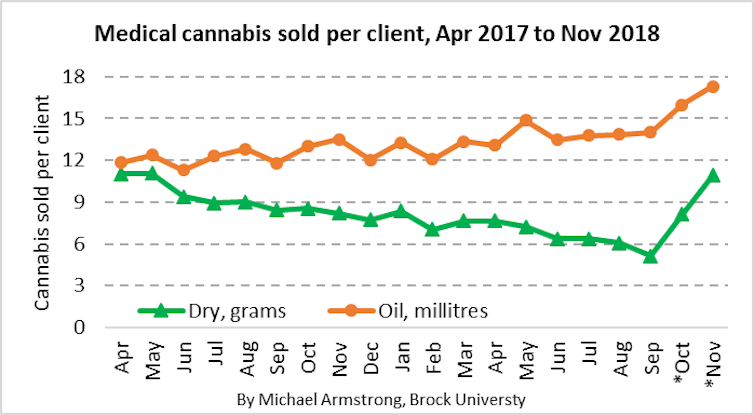

Consider medical cannabis. Between April 2017 and September 2018, oil sales per registered client increased 18 per cent. Meanwhile, dry sales plunged 53 per cent, from 11.0 grams per client to just 5.1.

Dry sales’ steep decline might reflect a gradual medical shift to oils. But shortages also might have contributed.

RELATED: Could Canada Use Nevada’s Marijuana Shortage Protocol?

The post-legalization sales increases support that theory. November’s oil sales were 18 per cent above September’s. But dry sales soared 103 per cent. Medical clients seemingly refilled their dry supplies after legalization made prescription transfers easier.

Differences between oil and dry cannabis also appear in the recreational cannabis data.

Oil flows, dry cannabis struggles

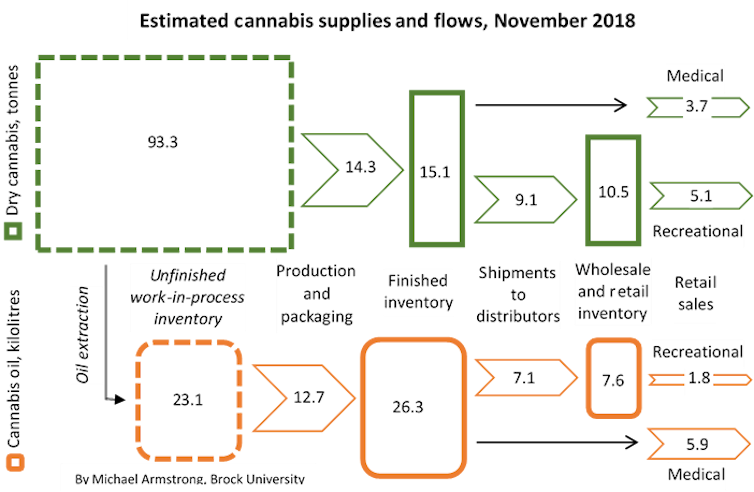

For cannabis oil, recreational sales hit 1.9 kilolitres in November, legalization’s first full month. But comparison to October’s stronger numbers suggests retailers lost sales of roughly 1.8 kilolitres due to shortages. That implies potential recreational demand was around 3.8 kilolitres monthly. Meanwhile, medical sales hit 5.9 kilolitres.

Distributor inventories ended November in good shape. They more than doubled to 7.6 kilolitres. That’s enough to satisfy more than two months of recreational demand.

Similarly, producers ended with 26.3 kilolitres of finished (ready-to-ship) oil. That’s nearly three months of combined recreational and medical demand. Plus, their production and outbound shipping rates both exceeded total end-user demand. That suggests shortages would ease over time.

By comparison, dry cannabis struggled in November. Sales were 5.1 tonnes, but lost sales were perhaps about 8.3 tonnes. That put monthly recreational demand around 13.4 tonnes. Medical sales hit 3.7 tonnes.

RELATED: Canadian Marijuana Shortages Could Go On For Years

Distributors’ inventory climbed significantly to 10.5 tonnes. But that’s insufficient for even one month’s demand.

Producer’s finished goods inventory of 15.1 tonnes likewise represented less than a month of combined recreational-medical needs. Production and shipments also trailed demand. That implies shortages would continue worsening.

Explanations?

Several explanations are possible for dry cannabis shortfalls existing despite large total inventories.

One is that 86 per cent of producers’ dry inventory was unfinished and not yet available for sale. Much of that was recent crops being dried and cured. But the large contrast with finished goods suggests possible processing and packaging bottlenecks too.

Another reason is these data add-up inventories across all producers. By contrast, each recreational customer is served by just one provincial distributor.

Suppose one source has a surplus while another has a shortage. Their total inventory could look healthy. But half their users would see empty shelves.

As well, supply and demand are much harder to balance for individual products than for overall product categories. That’s a common retail problem.

For example, imagine visiting a clothing store. Request “a shirt”, and sales staff could show you hundreds. But specify “a long-sleeved, medium-tall, all-cotton, emerald-green shirt” and they might have none to offer, despite huge inventory overall.

RELATED: Why Have Canadian Weed Companies Failed To Meet Expectations?

Cannabis buyers and sellers likely experienced such mismatches. Medical clients treating conditions like epilepsy would be especially at risk. They’d want specific product formulations, not random substitutes.

One factor that doesn’t look important is cannabis exports. In 2018, those averaged only 2.5 per cent of monthly production. That’s probably too small to significantly affect domestic availability.

Another non-issue was cannabis growing itself. Producers’ unfinished dry stockpiles remained almost unchanged during November. That suggests crop harvesting rates kept up with processing.

Bigger market, bigger challenges

The industry faces larger challenges longer term. Estimates of Canada’s total demand vary widely. But Health Canada’s latest assessment, for dry cannabis and oil equivalents combined works out to about 77 tonnes monthly.

So the legal cannabis industry must not only provide better availability of the specific products users want. To eventually serve every recreational and medical user, it also needs to massively grow its capacity. And it must do that while competing with black markets despite federal restrictions on branding and promotion.![]()

Michael J. Armstrong, Associate professor of operations research, Goodman School of Business, Brock University

This article is republished from The Conversation under a Creative Commons license. Read the original article.